Law Firms: Accounting Terminology

Law Firms: Accounting Terminology

Jan 22, 2022

Lawyers and Law Firms are often unfamiliar with accounting terms or find them strange. As a Law Firm, you need to know the Accounting terminology to be able to understand when your accountant is explaining your Finances.

In this post we will dive deep into educating the attorney on the most commonly used terms:

Assets

- An asset is a resource with economic value that a firm owns or controls with the expectation that it will provide a future benefit.

- Assets are reported on a company's balance sheet and are bought or created to increase a firm's value or benefit the firm's operations.

- An asset can be thought of as something that, in the future, can generate cash flow, reduce expenses or improve sales, regardless of whether it's manufacturing equipment or a patent.

Liabilities

- A liability is something that is owed to somebody else. Also, mean a legal or regulatory risk or obligation.

- In accounting, companies book liabilities in opposition to assets.

Accounting Methods

- Cash Basis: revenue is reported on the income statement only when cash is received and expenses are only recorded when cash is paid out.

- Accrual: means revenue and expenses are recognized and recorded when they occur, while cash basis accounting means these line items aren't documented until cash exchanges hands.

Cash basis is easier, but accrual accounting portrays a more accurate image of a Firm's health by including accounts payable and accounts receivable.

Tip💡

It’s important to separate the accounting method for books and for taxes. As a law firm, you probably manage your books in Accrual because this method gives you better information when making financial decisions. For Tax purposes, your preparer is probably using the cash method because it is usually the best option for small businesses. You pay taxes based on income that was collected and expenses that were paid. What is sitting in A/R and A/P does not affect your taxes.

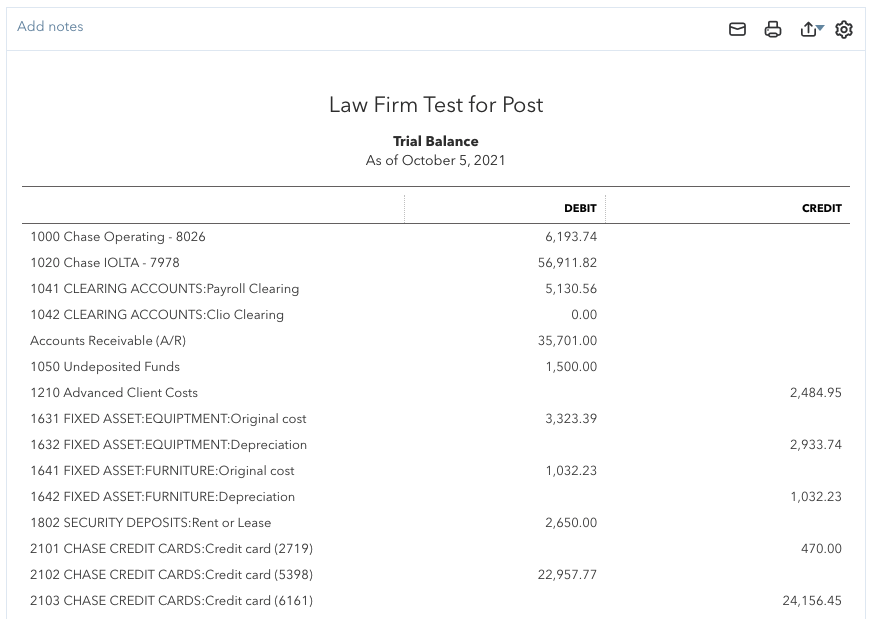

Balance Sheet

- A balance sheet is a financial statement that reports a Firm's assets, liabilities, and equity.

- The balance sheet is one of the three core financial statements that are used to evaluate a business. It provides a snapshot of a Firm's finances (what it owns and owes).

Profit & Loss or Income Statement

- A P&L is a financial statement that reports a Firm's income and expenses.

- The P&L is one of the three core financial statements that are used to evaluate a business. It provides a snapshot of a Firm's finances (what was the total income and total expenses for a given period).

Debits & Credits

- Debits are the part of the journal entry that increases an asset or expense account and decreases a liability or equity account. Accounts that increase when debited are found on the left side of the balance sheet and the trial balance and include Draws, Expenses, Assets, and Losses.

- Credits are the part of the journal entry that increases a liability or equity account and decreases an asset or expense account. Accounts that increase when credited are found on the right side of the balance sheet and the trial balance and include Gains, Income, Revenues, Liabilities, and Owner’s Equity.

We hope this information has been useful to you and has helped you understand a little more about accounting terms. If you need more guidance #ContactUs at [email protected]